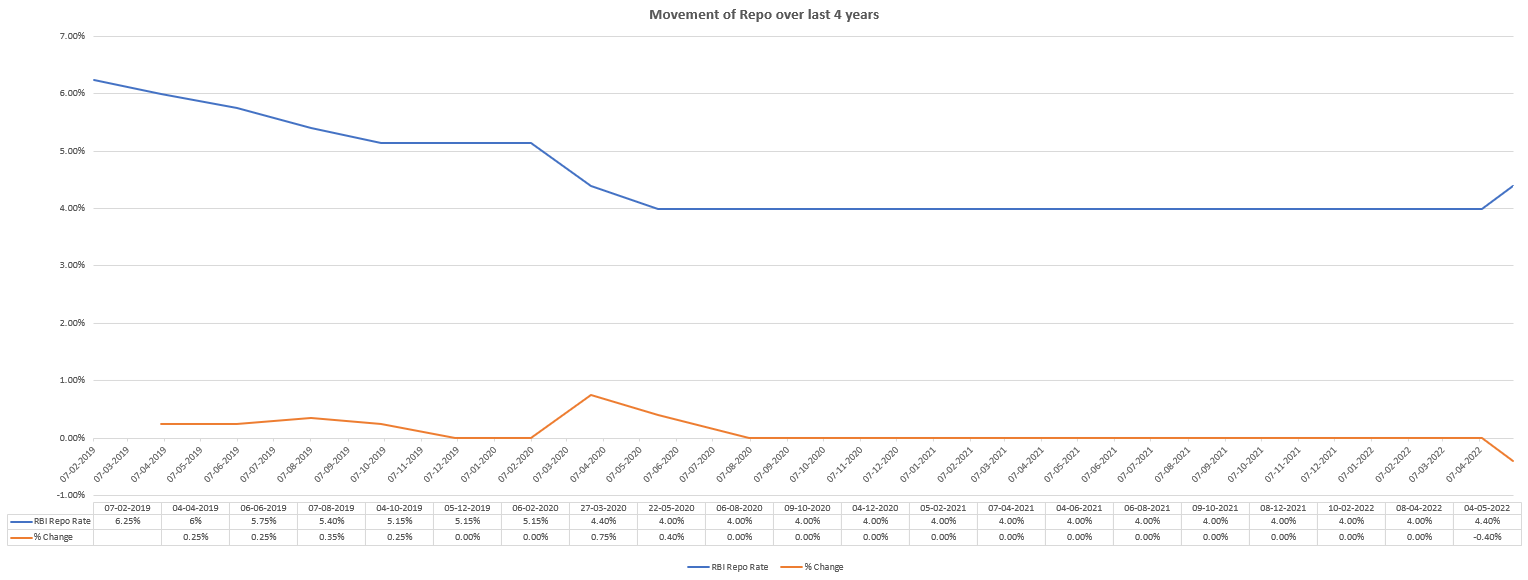

We can see in the above graph that RBI was constantly decreasing the rate to increase the money supply in the market. After the covid impact RBI has decreased it drastically, which can be seen in the % change in ...Read more

We can see in the above graph that RBI was constantly decreasing the rate to increase the money supply in the market. After the covid impact RBI has decreased it drastically, which can be seen in the % change in 2020. This was done to make funds cheaper for banks thus aiding them to bring down lending rates. RBI continued with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward”.

Now recently RBI increased it 4.40% but it was unchanged since 20th may 2020.

Read less