HDFC will acquire a 41 percent stake in HDFC Bank through the transformational merger, according to an HDFC Bank filing with the stock exchanges. The merger is expected to be completed by the second or third quarter of FY24. After ...Read more

HDFC will acquire a 41 percent stake in HDFC Bank through the transformational merger, according to an HDFC Bank filing with the stock exchanges. The merger is expected to be completed by the second or third quarter of FY24. After the merger, HDFC Bank will be 100 percent owned by public shareholders and existing shareholders of HDFC Limited will own 41 percent of HDFC Bank.

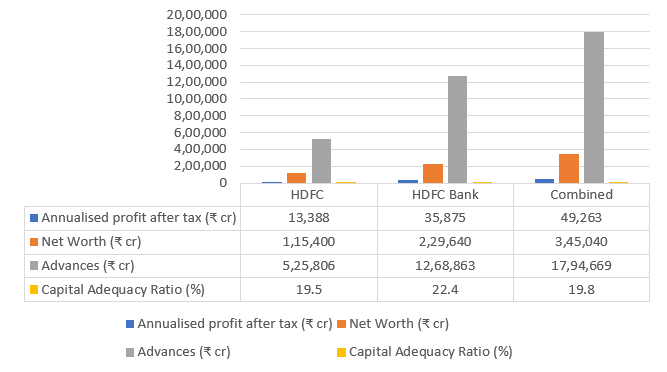

HDFC has total assets of Rs 6,23,420.03 crore, turnover of Rs 35,681.74 and net worth of Rs 1,15,400.48 crore as on December 31, 2021. HDFC Bank, on the other hand, has total assets of Rs 19,38,285.95 crore, turnover (includes other income) of Rs 1,16,177.23 crore for the nine months ended December 31, 2021, and a net worth of Rs 2,23,394.00 crore, as on December 31, 2021.

All Financial Experts & Institutions have different opinions, but are positive about the merger.

- A merger of HDFC and HDFC Bank would create the second largest financial entity in the country after SBI in terms of assets.

- The merger could create the second largest company in India by market capitalisation, leaving behind TCS, the crowning jewel of the Tata group.

- The share exchange ratio for the amalgamation of HDFC with and into HDFC Bank will be 42 equity shares, credited as fully paid up, of the face value of Re 1 each of HDFC Bank for every 25 fully paid-up equity shares of the face value of Rs 2 of HDFC.

- Merger will not impact employees of HDFC Ltd, said Deepak Parekh.